The security robot is already capable of patrolling on its own, day and night, in all weather conditions. It detects fires, gas leaks, and intrusions. This capability exists; it’s on the market; and it’s in use at real-world sites. And yet, the market hasn’t taken off. The problem, then, isn’t with the machine—it lies in how robotics engineers and security companies communicate with each other, understand one another, and do or do not build the trust necessary for adoption. This article unpacks this paradox and shows you where the real roadblock lies—and how to break through it before the window of opportunity closes.

A technically mature market, but commercially immature

Let’s start with an unsettling observation. On paper, the occupational safety and health industry is doing well. In 2023, the sector generated €11.12 billion (excluding tax), a 10% increase compared to 2022—a growth rate that attests to the sector’s strong performance at the national level. Demand is there. Employment is also on the rise: the sector employed 210,500 workers at the end of 2023, a 2.5% increase from the previous year, and more than 200,000 workers were active in 2025.

So much for the facade. Behind it, the picture is turning dark—and fast.

Because the growth in revenue masks a formidablesqueeze effect. There are two reasons for this. On the one hand, wages are skyrocketing: since the end of the COVID pandemic, employers’ organizations have taken action to keep pace with the general trend in wage levels, resulting in a 20% increase in just four years. On the other hand, customers are refusing to absorb these increases. The GES secretary general acknowledges this bluntly: there is a great deal of reluctance on their part, which has a direct impact on the sustainability of certain services.

As a result, profit margins are shrinking. Under the combined effect of falling rates imposed by clients and rising social security contributions, profit margins are narrowing dangerously, particularly for very small businesses and SMEs, which nonetheless form the backbone of the market. The GES even issued a public warning about this in late 2025: the rising costs faced by private security firms are not being passed on to the market, putting the sector in increasingly dire straits.

Compounding this pressure on prices is a human crisis. Generational turnover is expected to be difficult: nearly 30% of employees are over 50, highlighting a generational turnover challenge ahead. And employee turnover is like a silent hemorrhage: the private security sector in France has an annual staff turnover rate of 22%, which is a record high compared to the national average of 15.5% in 2024.

This turnover is a direct financial burden. Hiring a new private security guard costs an average of between 3,000 and 5,000 euros, including recruitment costs, interviews, equipment, and the onboarding period. Consider a well-structured small-to-medium-sized enterprise (SME) with 350 agents—one that has its own major clients and does not operate solely as a subcontractor: with a turnover rate of 22%, it must replace nearly 77 agents each year. The recruitment cost alone exceeds 300,000 euros annually, not to mention the operational disruption and the perceived decline in service quality experienced by the client. The vicious cycle is complete: employers struggle to attract and retain their workforce, while employees—often in precarious positions—oscillate between disillusionment and forced job mobility.

It is precisely this company that has the most to gain. Large enough to manage its own contracts and clients, it is also mature enough to see the robot as more than just a threat: a tool for retaining and upskilling its agents. Where a small subcontractor sees only an expense, the SME with 350 agents sees a direct solution to its HR drain and a way to shift its teams toward higher-value tasks.

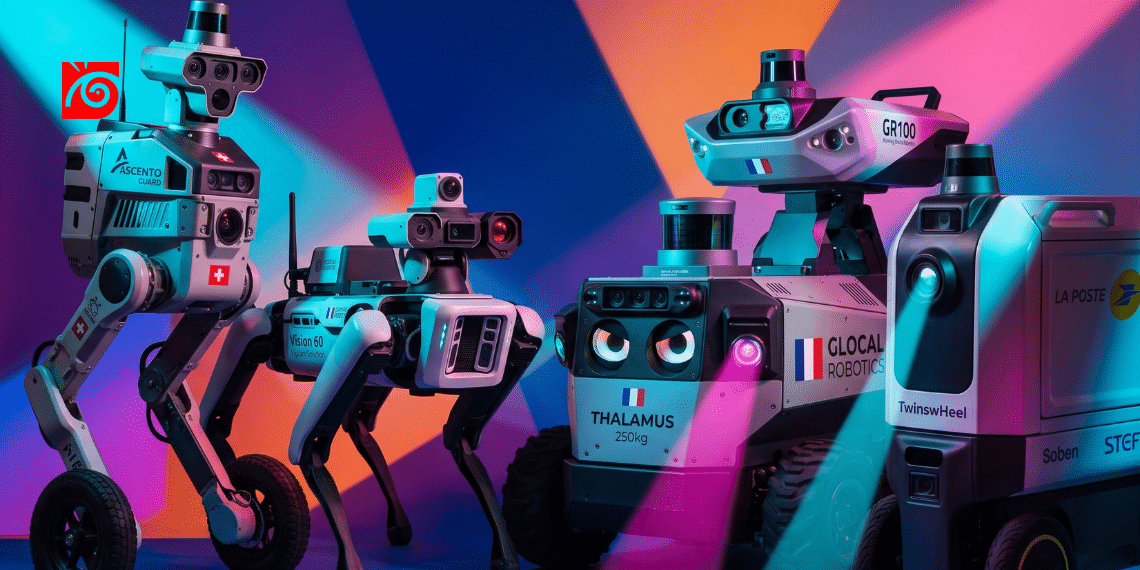

Faced with this challenging economic reality, what do we find? Machines that can already do everything. The robot patrols completely autonomously, day and night, in all weather conditions. The GR100, a French-designed robot, exemplifies this level of maturity.

The conclusion is obvious.The problem is not technical. It lies elsewhere.This is precisely the kind of trap we describe in our analysis ofthe “techno-push” versus strategic value in deep tech: an engineering feat does not automatically create a market. Value must be articulated, not merely demonstrated.

Panorama: Five Actors, All Showing the Same Level of Maturity

There’s no need to compile a product catalog. What matters is what the simultaneous emergence of these players reveals. Several teams, working from different technological, geographic, and economic foundations, have arrived at roughly the same functional building block. That’s the real sign:technological maturity is no longer a hypothesis—it’s a proven fact.

Let's go over them.

GR100 (Running Brains Robotics): The All-Weather Autonomous Patrol Robot

The GR100 is a French robot designed for industrial sites and unique locations. The GR100 is a fully autonomous robot designed to patrol the exterior of buildings at an industrial site. It performs two distinct tasks: security—it detects people and vehicles and alerts the security post in the event of an intrusion. The guard station responds quickly by taking control of the robot to assess the intrusion. For safety purposes, the robot performs specific site checks (thermal imaging, gas leak monitoring, meter and gauge readings, and verification of door and gate closures) and alerts personnel in the event of an abnormal situation.

Why the technology is mature:The robot patrols completely autonomously, day and night, in all weather conditions. And humans remain in control: The inspection robot can be remotely operated by an operator so that it can safely investigate suspicious situations. Most importantly, the GR100 is not a lab prototype. It patrols around the clock, deterring intruders and detecting any anomalies at an airfield, where a manager notes: “The GR100 has truly found its place here.”

Ascento Guard (Ascento): The Swiss All-Terrain Bipedal Robot

In Switzerland, ETH Zurich spin-off Ascento has raised $4.3 million and announced the launch ofAscento Guard, its new autonomous robot that serves as a security guard. Its unique feature is its mechanical design: the robot consists of two wheels and two foldable legs that allow it to move across any type of terrain, including stairs.

Why the technology is mature:its functions already cover a wide range of applications. In addition to monitoring parking lots, it can detect floods and fires, control lighting on properties, verify that doors and windows are closed, detect criminals or unauthorized visitors, and check the integrity of a given perimeter. Deployment is rapid, and the solution integrates with existing infrastructure: the Ascento app uses AI for video analysis, integrates with existing systems, provides secure communication, and generates customized reports for security managers. Once again, real-world results speak for themselves: designed to provide deterrence, monitoring, and detection, Ascento Guard autonomously patrols the parking lots at Lyon Airports.

THALAMUS (Glocal Robotics): The Heavyweight, Mature, Yet Breakthrough-Capable Goalkeeper

The THALAMUS is a large-scale French robot developed by Glocal Robotics, a company based in Angoulême. This massive security robot weighs 250 kg, and that weight is no small matter: the robot’s 250 kg mass gives it the stability needed to continue operating under any circumstances. Designed in France, THALAMUS is an autonomous security robot intended for securing sensitive sites; versatile, it combines safety and industrial security.

Why the technology is mature.Equipped with sensors, the THALAMUS conducts surveillance patrols completely autonomously for about a dozen hours on a single battery charge. Its perception capabilities are advanced: thanks to its sensors (LiDAR + high-resolution camera + thermal camera) connected to two artificial intelligence (AI) modules, the THALAMUS can detect an intruder, alert authorities to an incident, deter threats, or even intervene. A key factor in its operational credibility is its use of AI to analyze situations and reduce false positives. R&D continues: the 2026 models incorporate new positioning technology developed by the Swiss company Fixposition to improve navigation accuracy. This is therefore a product at the highest level of maturity (TRL9), still in development.

Where THALAMUS is actually being used—and what that reveals.The technology is mature; however, its adoption is taking place elsewhere than one might expect. Three documented deployments illustrate this:

- The French military, not private security firms.The THALAMUS was deployed during the ORION 2026 exercise to secure a strategic infrastructure, a deployment led by the distributor SCOPEX. Renato Cudicio points out that the robot frees military personnel from repetitive surveillance tasks, allowing them to focus on high-value-added missions that require human judgment and expertise.

- A foreign systems integrator, in an urban civilian environment.THALAMUS conducted a successful demonstration in Nordelta, a private city on the outskirts of Buenos Aires, as part of a three-dimensional air-land-sea security ecosystem designed by the Argentine systems integrator Securion. A genuine civilian deployment, but by a foreign systems integrator, not a French private security agency.

- North American expansion is underway.THALAMUS has officially joined the Glocal Robotics team in Quebec, with the goal of adapting the product to the demands of the North American market and Canadian climate conditions.

Keep this case in mind, as it sets the stage for the next section.Glocal Robotics aims to become the European leader in security robotics within its segment within five years. However, its product—though mature—is initially gaining traction with the military and international integrators, rather than with French private security firms. This discrepancy is no minor detail. It isliving proofof the thesis of this article.

Vigilant Solution: The Quadruped Robot, the French Dual Integrator

Vigilant Solution occupies a unique position in this landscape. The company doesn’t just manufacture another machine: it is aFrench systems integratorwhose stated mission is to provide robust and reliable robotic solutions that you can trust over the long term. What sets it apart is the platform it has chosen. Its perimeter security solution is based on the Vision 60 robotic platform, the quadruped robot (the “robot dog”) renowned for its all-terrain agility. Another unique feature is its openlydual-use positioning, serving both the defense sector (reconnaissance, perimeter security) and the industrial sector (surveillance, monitoring).

Why the technology is mature.In terms of perception, it is on par with other players in the market. Equipped with a high-performance thermal camera, the robot ensures precise surveillance, even at night or in foggy conditions, and by incorporating the latest artificial intelligence algorithms, it detects threats in real time. Its navigation is operational-grade: it can operate autonomously, without GPS or a network, while its RTK positioning system ensures precise positioning to within 10 cm. As with other systems, the human operator retains control: if necessary, you can take manual control of the robot at any time to perform precise and immediate interventions.

The added benefits of the quadruped design.Where a wheeled robot reaches its limits, the quadruped design goes beyond them. The robot remains operational in extreme weather conditions—whether snow, intense heat, or wet terrain—and effortlessly traverses rugged, sandy terrain or even dunes. It also enables missions that no fixed camera can cover: it is capable of exploring and monitoring tunnels or underground passages, and quickly detecting breaches or anomalies in perimeter fences.

This is what Vigilant Solution demonstrates in support of our thesis.Its approach—which focuses on integration rather than building a proprietary robot—reveals a core belief: the key isn’t the mechanics; it’s the ability to integrate into the customer’s existing infrastructure. Their solution integrates seamlessly with centralized video surveillance systems and can be controlled via a PC, tablet, or smartphone. In other words, Vigilant is selling not so much a robot as atrusted integration solution. This is precisely the shift this article advocates.

TwinswHeel (Soben): The Hypercenter Droid, and Proof Through Legal Lockdown

TwinswHeel stands apart, and that is precisely what makes it so crucial to our demonstration. It is a French brand founded in 2016 by Vincent Talon and Benjamin Talon, backed by the Cahors-based SME Soben, whose entire production chain—from raw materials to assembly—takes place locally, near Cahors. Its specialty isn’t closed-course testing, but rather the most demanding terrain imaginable for a mobile robot: autonomous last-mile delivery in dense urban centers.

This is why it’s the most advanced robot in dense public environments.Navigating a city center—amidst pedestrians, bicycles, and street furniture—is infinitely more complex than patrolling a fenced-off perimeter. Yet TwinswHeel is already operating there. Several small follow-along robots are crisscrossing downtown Toulouse alongside Enedis technicians, carrying the equipment needed for the technicians’ work on the power grid right behind them. And fully autonomous operation in urban areas has become a reality: in Montpellier, La Poste and Stef, the European leader in refrigerated transport, are testing last-mile delivery using fully autonomous robots. At the initiative of the Montpellier metropolitan area, a 36-month trial with autonomous robots began in 2021. The navigation technology is mature: maps are generated using SLAM (simultaneous localization and mapping) algorithms and redundant perception sensors.

Why the real obstacle isn’t technical.At TwinswHeel, the machine works. What’s holding it back is the regulatory framework. Regulations require a “safety driver”—a driver capable of taking control of the robot at any moment in the event of an incident, via a 4G or 5G connection. And these virtual routes must be safely defined and approved by national and local regulators.

Keep this case in mind.At TwinswHeel, it’s not the robot that’s holding things up—it’s regulations and public acceptance. The proof? The company has made overcoming this hurdle its top priority: TwinswHeel is the only French company authorized to conduct such experiments, which are being carried out as part of the SAM project (Safety and Acceptance of Autonomous Driving and Mobility), the consortium that won ADEME’s EVRA (Experimentation with Autonomous Road Vehicles) call for projects, alongside players such as Renault, Stellantis, RATP, and SNCF. The goal: to develop regulations for autonomous vehicles in urban areas. The technology is waiting for the law and public trust to catch up.That is precisely the thesis of this article.

What this overview shows

Actor Origin Favorite spot Proof of Maturity GR100(Running Brains) France Industrial sites, airfields 24/7 all-weather patrol, gas and thermal detection, deployed in the field Ascento Guard(Ascento) Switzerland Parking lots, perimeters, mixed-use sites All-terrain bipedal robot with fire and flood detection capabilities, deployed at Lyon Airports THALAMUS(Glocal Robotics) France (Angoulême) Sensitive sites, defense, international system integrators 250 kg, dual-module LiDAR + AI, Fixposition 2026 positioning system; deployed at ORION 2026 in Nordelta, Argentina; expanding into Quebec Vigilant Solution France (system integrator) Industrial and defense (dual-use) sites, extreme environments Plateforme quadrupède Vision 60, caméra thermique + IA temps réel, localisation RTK <10 cm, autonomie sans GPS ni réseau TwinswHeel(Soben) France (Cahors / Rhône) Dense urban hub, shared public space SLAM + sensor redundancy, autonomous delivery in Montpellier; legal hurdles (safety driver, regulatory approval)

The conclusion is clear. Five teams, two countries, different architectures, the same result. When convergence is this clear, the question is no longer “Is it feasible?” but “Why isn’t the market buying it yet?” The bottleneck isn’t innovation—it’s adoption.This is the crux ofthe technological continuum between defense and private security, where mature technologies struggle to find their place due to the lack of a clear use case. And the TwinswHeel case proves it all on its own: sometimes, the last hurdle isn’t technical—it’s legal and cultural.

The need that no one has yet been able to articulate

This is the crux of the misunderstanding.

Most security companies view robots through a single lens:job replacement.“How many agents will this machine replace?” The question seems rational. In reality, it is deadly—for two reasons.

First, it creates fear, both internally and among customers. Second, it confines the calculation of ROI to a scope that is far too narrow: that of payroll savings. Yet in an industry where margins are already being squeezed by the squeeze effect, this line of reasoning leads only to risk-averse accounting decisions.

The real need lies elsewhere. It islatent, unspoken, and vital.

This need is to create anew line of services with higher margins, one that can be sold to the end customer as a move upmarket. Not “I’m replacing two agents with a machine,” but “I’m offering you enhanced, traceable, round-the-clock monitoring that your competitors can’t yet provide.” In an industry where operating costs can no longer be passed on to prices, this isn’t just a technological gimmick. It’s a lifeline.

And if you still doubt that the problem lies anywhere other than in the machine, look for this telltale sign:where do orders for the best products actually go?

Take Glocal Robotics’ THALAMUS. Technically, it’s one of the most advanced French security robots. Yet its most solid documented deployments aren’t with French private security firms. Instead, they include the French military through the ORION 2026 exercise, an Argentine integrator for a private city near Buenos Aires, and a North American expansion in Quebec. In other words: the product is gaining traction with the military and internationally, but is struggling specifically in the French private security sector.

This observation is troubling—and highly revealing. If such a mature product does not immediately gain traction where the economic need is so pressing, it is clear thatthe obstacle is not the machine’s performance.The obstacle is the market’s inability to articulate the need, recognize the value, and build trust. Buyers who can already articulate their need—such as a military organization or a structured systems integrator—are making purchases. Those who have not yet learned to recognize the value, despite an economic urgency, remain on the sidelines. Technology waits for no one; it is the commercial maturity of the segment that is lacking.

The challenge? Buyers don’t spontaneously express this need. This is the crux ofthe matter when it comes to the autonomy of B2B buyers and their purchasing journey: customers proceed on their own, using their own criteria, and will never buy a value they haven’t been taught to recognize. The supplier’s role is no longer to “present a product,” but toreveal a need.

This inability to translate technical capabilities into perceived value comes at a cost. We analyzed this in our breakdown ofthe cost of strategic ambiguity for SMEs: the lack of a clear narrative results in lost margins, extended sales cycles, and proof-of-concept projects that never come to fruition.

The Invisible Value on Both Sides of the Market

The impasse is symmetrical. Robotics engineers and security firms are each facing an obstacle they do not name.

From a robotics engineer's perspective: the real obstacle isn't AI—it's trust

Engineers think in terms of performance: detection range, false positive rate, battery life. These are real criteria, but they don’t close the sale.

Three non-technical obstacles carry much more weight:

- The Legal Framework.Private security is a highly regulated profession. It is governed by a robust legal framework, set forth in Book VI of the Internal Security Code. This text defines the essential rules: who can become an agent, what their daily obligations are, and what penalties apply in the event of a violation. However, this framework was designed for human agents certified by the CNAPS. Where do robots fit in? The TwinswHeel case demonstrated this earlier: sometimes, the only real obstacle is regulatory.

- Cultural skepticism within the profession.The sector is rooted in a culture of hands-on work, human presence, and personal responsibility. Autonomous machines are not adopted here simply out of enthusiasm for technology.

- The lack of documented lessons learned.Without tangible evidence from a peer, the executive will not take responsibility. The case of THALAMUS illustrates this: its most visible references are military or foreign, which precisely deprives French private security companies of a “mirror” set of lessons learned with which to identify.

The robotics engineer who sells a spec sheet loses. The one who builds trust wins. This is the logic behind our focus onaugmented intelligence rather than replacement: technology is adopted only when it becomes part of a business culture, not when it claims to replace it.

From a security company's perspective: Robots are not a threat; they are a tool for human resources

The agent’s defensive reaction is understandable: “The machine is going to take my job.” But this line of reasoning turns reality on its head.

The robot precisely takes on the tasks that are exhausting and drive people away. The GR100 automates the tedious and repetitive tasks of security guards: repetitive night patrols, perimeter checks in rainy weather, and mechanical door inspections. What the machine does not do is interpret, build relationships, or make decisions. These tasks remain the domain of humans, and they are the most rewarding. This principle even applies to defense: during Exercise ORION 2026, one of the robot’s major contributions was freeing military personnel from repetitive surveillance tasks, allowing them to focus on high-value-added missions requiring human judgment and expertise.

The robot's manufacturer says it itself: having robots work alongside human security guards helps solve problems such as high staff turnover and low profit margins for security companies.

In other words, when deployed effectively, the robot becomes atool for employee retention. It enhances the value of the agent’s role, reduces the physical strain of the job, and tackles at its root the 22% turnover rate that is weighing down the industry. For the SME with 350 agents mentioned above, the equation is crystal clear: rather than replacing 77 agents each year, it uses the robot to retain its best employees and promote them to roles such as operator, supervisor, or case resolution specialist—positions that are more skilled and better valued. We’ve analyzed this battle to enhance job value in the contextofthewar for talent and employer branding: you don’t retain talent with salary alone, but with a sense of purpose and better tools.

The Strategic Compass: A Shared Negotiating Table

At this point, one thing becomes clear: robotics engineers and security firms want the same thing—to drive adoption—but they don’t speak the same language. One thinks in terms of performance and development cycles; the other in terms of profit margins, scheduling, and legal liability. The result: two worlds that intersect without understanding each other, and a sale that never goes through.

There is no common framework. Nonegotiating tablewhere each side can see what the other stands to gain. That is the purpose of the Strategic Compass: four pillars, viewed simultaneously by both sides, to transform a dialogue of the deaf into a shared project.

Let's go over them one by one, because it's the details that make or break the adoption.

Pillar 1: The Governance Foundation—Decide Before You Buy

For the robotics engineer.The first mistake is to sell a machine. The right approach is to clarify a strategic positioning: the robot is atool for augmentation, not a tool for replacement. This choice is not merely cosmetic. It determines the sales pitch, pricing, product narrative, and even the design of the human-machine interface. A robotics engineer who hasn’t resolved this issue sends mixed signals and loses the buyer’s trust even before the demonstration begins.

For the security company.The robot isn’t a one-off purchase—it’s acorporate strategy decision. Introducing an autonomous machine into your service offering means choosing to evolve your business model, your value proposition, and your customer relationships. This is a decision made at the executive level, not by a division manager who’s “testing out a gadget.” Without clear direction from the top, the project remains an orphaned proof of concept that will be shelved at the first sign of budget constraints.

The common ground:for both sides, the key question is not “which machine?” but “which strategy?” That is precisely the role ofthe Governance Framework: to establish the vision before committing resources.

Pillar 2: The Influence and Authority Engine—Proving and Storytelling

For the robotics engineer.A technical spec sheet won’t convince anyone in a skeptical industry. What does convince isdocumented evidence: real-world use cases, quantified feedback, and peer testimonials. Robotics engineers must become producers of authoritative content, not just sellers of specs. Every successful deployment must be leveraged, shared, and publicized. That’s how you establish yourself as a market leader in an emerging sector—before competitors do.

For the security company.The robot has value only if it canbe sold to the end customeras a premium upgrade. But you still have to know how to sell it. The security company must craft a narrative that transforms technical capabilities into perceived benefits: “enhanced surveillance,” “complete traceability,” “service continuity that no competitor offers.” Without this narrative, the robot remains an internal cost rather than becoming a differentiating sales pitch.

The common ground:both parties need to build evidence and a narrative—one to sell the robot, the other to sell the augmented service. This is the mission ofthe Influence and Authority Engine: to produce the content, SEO, and visibility that transform a technology into a market authority.

Pillar 3: Trust Capital, the key that controls everything else

This is where it all comes down to. Withouttrust, none of the other pillars can stand.

For the robotics engineer.The real obstacle is neither AI nor the battery: it’s thelegal uncertainty and the issue of liability. Who is liable if the robot fails to detect an intrusion? How does the machine fit within the Internal Security Code, which was designed for humans certified by the CNAPS? As long as these questions remain unresolved, the executive won’t sign off on it, regardless of the advertised performance. The robotics engineer must therefore anticipate, define, and address these blind spots—just as TwinswHeel has made removing regulatory barriers its top priority.

For the security company,the key lies with people. We needto get the agents on board and turn fear into support. An agent who perceives the robot as a threat will sabotage it, either passively or actively. An officer who is told that the machine alleviates the drudgery of the job and helps them develop their skills will become its best advocate. This shift cannot be imposed; it must be prepared for, communicated, and supported.

The common thread:agent mistrust, regulatory ambiguity, and a lack of evidence—all point to the same need forreassurance. And reassurance can’t be improvised; it must be managed. That is precisely the purpose of“Capital Confidence and Experience”: to secure accountability, build on lessons learned, and manage perception and acceptability. This is the pillar that makes all the difference.

Pillar 4: The Internal Culture Engine—Embedding Change

For the robotics engineer.You don’t sell technology in opposition to a culture; you sell it alongside it. The robotics engineer mustunderstand the target industry’s culture: the importance of human presence, the logic of the field, and the relationship to personal responsibility. A product designed in a vacuum, without this understanding, will be rejected regardless of its quality. Industry empathy is a business asset, not just a nice-to-have.

For the security company.The robot only delivers its full value if it becomes atool for employee retention and purpose. For the SME with 350 employees mentioned above, the challenge is not to eliminate 77 positions per year, but to retain its best employees by promoting them to roles as operators, supervisors, or incident investigators. The robot then becomes an employer-branding tool, a selling point in a sector facing chronic labor shortages.

The key point:Sustainable adoption isn’t about the purchase itself, but about the cultural integration that follows. That’s the role ofthe Culture and Internal Growth Reactor: to make the robot a driver of corporate culture and customer loyalty—on both sides of the table.

An Overview

Strategic pillar For the robotics engineer For the security company Governance Framework Clarifying Your Positioning: A Tool for Growth, Not a Replacement Decide on a supply strategy, not a one-time purchase Influence & Authority Engine Document use cases, provide evidence Communicate the move to a higher-end product to the end customer Trust Capital Clarify the legal uncertainty and provide reassurance regarding liability Get employees on board; turn fear into commitment In-house reactor Understanding the Target Business Culture Using the robot as a tool for retention and purpose

One thing is clear from this picture. The four pillars are not à la carte options: they form a system. But they do not operate in a haphazard manner. Governance sets the course, influence produces evidence, and culture anchors change. And at the center,trust is the foundation for everything else. Mistrust among employees, regulatory uncertainty, and a lack of evidence—all of these factors point to a single need for reassurance. And this reassurance, let’s reiterate, cannot be improvised. It must be actively managed.

Conclusion: A Short Window of Opportunity

Let’s recap. The technology is ready, proven, and deployed at real-world sites. The market, however, remains stalled—not because of the technology itself, but due to a lack of narrative and trust on both sides. Security companies see it as a cost when they should see it as a new source of profit, in an industry where the GES has warned that costs are no longer being passed on to prices. Robotics companies are selling performance when they should be building relationships. THALAMUS epitomizes this: an excellent French product that is gaining traction with the military and internationally, but remains on the sidelines of the French private security sector due to a lack of trust.

This status quo won’t last. There are currently four or five serious players in the market. Within two to three years, there are only two possible scenarios: either a standard will emerge and reshape the market, or the sector will remain trapped in a series of short-lived proof-of-concepts.Technology won’t wait for anyone. It’s strategy that needs to catch up.

But this delay isn’t an engineering problem. It’s a matter of trust, experience, and perception—exactly the domain ofCapital Confiance & Expérience. Building reassuring feedback loops, clarifying the narrative amid legal uncertainty, engaging agents rather than alienating them, and transforming technical capabilities into a perceived upgrade for the end customer: that’s where adoption is won—or lost.

👉Are you a robotics engineer whose technology isn’t translating into contracts? Do you run a security company and want to create a compelling premium offering?Find out how the Capital Confiance & Experience offer transforms a technical feat into a sustainable business advantage by addressing the only barrier that truly matters: trust.